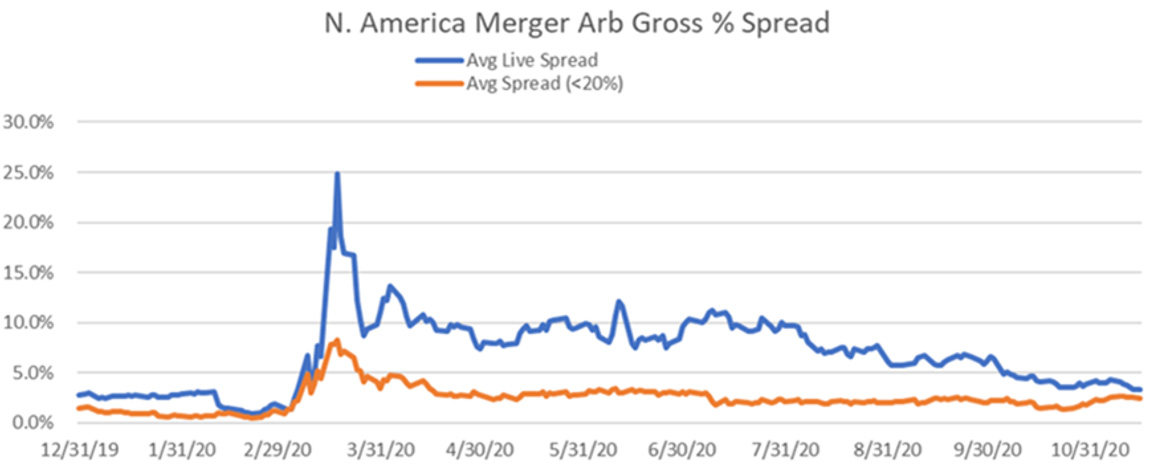

With the recent merger arbitrage litigation settlement in the REIT sector, the event driven space has closed the books on one of the most unique times to invest in Risk Arbitrage. As the pandemic began to rip through all our lives, merger arbitrage spreads widened significantly. The average spread across North American deals went from approximately 1% in early February, to a peak of over 20% at the depths of the pandemic crisis. In addition to general risk off in the markets during 1Q2020, arbitrage investors had to contend with a slew of companies facing a serious case of buyer’s remorse, looking for any angle to break their definitive merger agreement.

Source: MS Special Situations, Public Filings, Bloomberg

Assessing the landscape of the 55 ‘live definitive deals’ in mid-February, of those that came into question, the tally was:

20% ended up breaking contract

* Eleven total breaks

* Six recuts

* Five permanent breaks

Ultimately, the primary driver of the arbitrage situations was buyer willingness to close the deal, even more so than the strength of the DMA and MAC carveouts. In the end, those buyers who wanted out worst, employed every tactic available to them, including forcing litigation.

The Driehaus Event Driven Strategy approach to risk arbitrage investing has always placed an emphasis on the strategic rationale of a deal and the buyer’s conviction in the merits of the deal. Deals with sound rationale, consummated at reasonable prices and with strong fundamentals underpinning the pro forma entity, stand to be consummated with a high probability of success. Certainly, strength of contract is an important, and crucial, component of merger arbitrage positions. However, as we’ve seen during this unprecedented period in 2020, a hesitant buyer is a difficult obstacle to deal with. In the end, it is the combination of a successful checklist of items that make the strongest merger arbitrage situations – committed buyer, strategic rationale, durational assets, strong contract - and ones that will continue to be a focus for the strategy.

This information is not intended to provide investment advice. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, market sectors, other investments or to adopt any investment strategy or strategies. You should assess your own investment needs based on your individual financial circumstances and investment objectives. This material is not intended to be relied upon as a forecast or research. The opinions expressed are those of Driehaus Capital Management LLC (“Driehaus”) as of November 2020 and are subject to change at any time due to changes in market or economic conditions. The information has not been updated since November 2020 and may not reflect recent market activity. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Driehaus to be reliable and are not necessarily all inclusive. Driehaus does not guarantee the accuracy or completeness of this information. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Other Commentaries

Driehaus Event Driven Fund March 2024 Commentary with Attribution

By Yoav Sharon

Driehaus Event Driven Fund December 2023 Commentary with Attribution

By Yoav Sharon