China’s slowdown is nothing new for investors, and the market seems to accept the “L-Shaped” growth story. However, the most recent money supply and credit data from the People’s Bank of China (PBoC) has raised new concerns about the ongoing adjustment process in the world’s second largest economy.

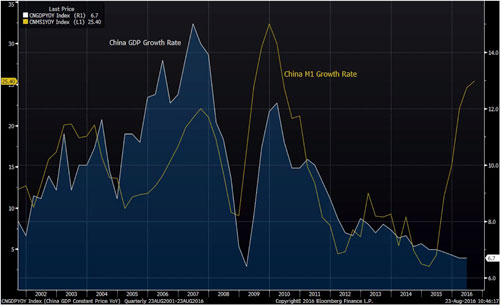

The money supply metric M1 is defined in China as the sum of currency in circulation and corporate demand deposits. Historically, growth in M1 has been highly correlated with GDP growth, leading many to use it as an indicator of China’s economic health. However, since mid-2015 the two metrics have diverged meaningfully (Exhibit 1).

Exhibit 1: Until recently, the rate of growth of M1 and China GDP were highly correlated

Source: Bloomberg

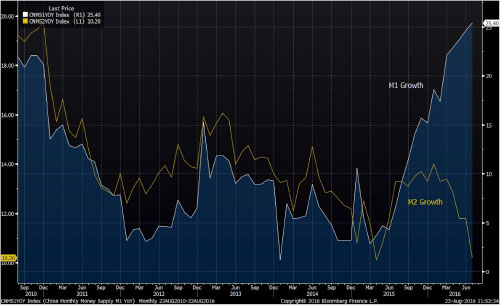

Over the same period, a similar divergence arose between M1 growth and the broader M2 growth, which includes saving deposits from corporates, the government and individuals. This is the most extreme instance of divergence between these series in the past two decades (Exhibit 2).

Exhibit 2: Why the recent divergence in China’s M1 and M2 growth?

Source: Bloomberg

Three possible reasons may explain the unusual concurrence of a surge in M1 with slowing growth of both GDP and M2.

Corporates may favor keeping cash at hand instead of investing it due to decreasing investment returns in the non-financial sector. Corporate demand deposits accounted for roughly half of the existing M1 and have contributed the majority of newly added M1, according to the breakdown analysis. The historically low fixed asset investment growth rate in July of 8.1% (YoY) and a slumping private investment growth rate of 1.5% (YoY) support this view.

A property market boom in tier one and some tier two cities may also have led to M2 growth decreasing and M1 growth soaring as household demand and saving deposits (calculated as M2) were transformed into demand deposits by property developers (calculated as M1) via pre-sales. Such a trend was verified by China’s July credit data, as it showed almost all new household loans went to the property market while corporates stopped borrowing, leading the total new loan (household plus corporate) in July to decrease 70% YoY.

Lastly, it is plausible that accounting and one-time factors also contributed to the divergence. For example, China’s Ministry of Finance’s debt-bond swap plan and government investment generated a temporary balance in corporate demand deposits, which was temporarily calculated as M1.

China’s monetary mystery is one manifestation of the unprecedented difficulties the country faces as it looks to shift its economy from investment to consumption driven. Namely, the value of previously reliable economic indicators and levers is eroding at a time when the property market is fevered, leverage is elevated, and both manufacturing investment and consumption are sluggish. Monetary policy, for its part, seems to have diminished in effectiveness, and China’s ability to adopt multiple approaches to push forward structural reforms while maintaining short-term growth must be monitored carefully.

This information is not intended to provide investment advice. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, market sectors, other investments or to adopt any investment strategy or strategies. You should assess your own investment needs based on your individual financial circumstances and investment objectives. This material is not intended to be relied upon as a forecast or research. The opinions expressed are those of Driehaus Capital Management LLC (“Driehaus”) as of September 2016 and are subject to change at any time due to changes in market or economic conditions. The information has not been updated since September 2016 and may not reflect recent market activity. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Driehaus to be reliable and are not necessarily all inclusive. Driehaus does not guarantee the accuracy or completeness of this information. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Other Commentaries

Driehaus Emerging Markets Small Cap Equity Strategy March 2024 Commentary With Attribution

By Chad Cleaver, CFA

Driehaus Emerging Markets Growth Strategy March 2024 Commentary with Attribution

By Howie Schwab